RHMI Humane Portfolio Model results updated through May 1, 2024

We’ve updated our RMHI Human Portfolio model results with the data through May 1, 2024.

Access our RMHI Humane Portfolio Model Data

We’ve updated our RMHI Human Portfolio model results with the data through May 1, 2024.

We’ve updated our RMHI Human Portfolio model results with the data through April 1, 2024.

We’ve updated our RMHI Human Portfolio model results with the data through March 7, 2024.

We’ve updated our RMHI Human Portfolio model results with the data through December 31, 2023.

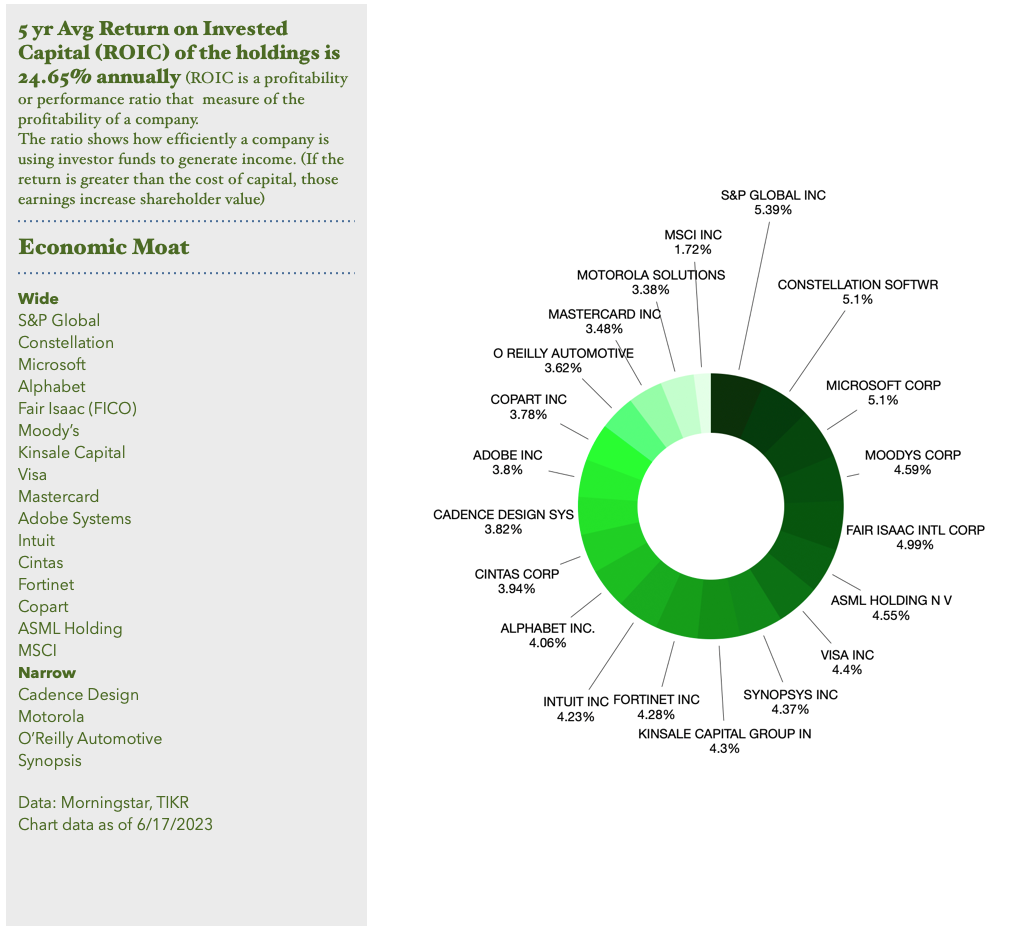

RMHI is a Colorado based state registered investment advisor that manages portfolios for Balanced and Growth investors. RMHI established the first Cruelty Free Investing policy in the US in 1996. RMHI manages a concentrated investment strategy that focuses on Free Cash Flow factors. To be considered for investment a company must have consistent free cash flow growth, maintain positive free cash flow margins and consistent Returns on Invested Capital (ROIC) above 15% on average. We add one technical measure of the stock’s stability relative to the S&P 500 over at least a decade. We prefer stability over volatility. Our goal is to minimize capital gains and transaction expenses by focusing only on companies that are capable of compounding value internally and by share price over a multi-year period.

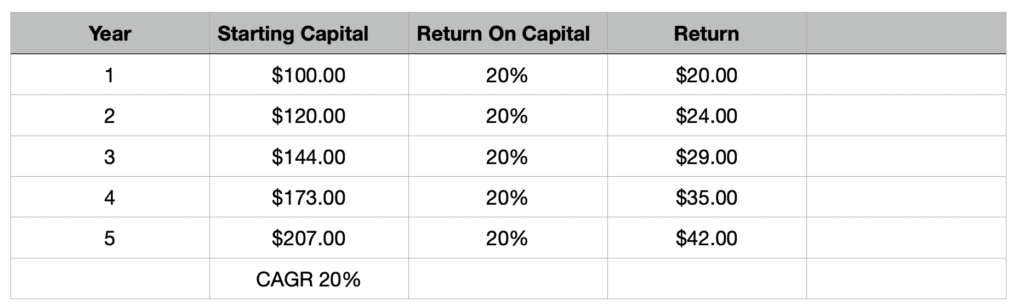

One of the most common questions I receive is “Why is it better to receive little or no dividends on my stocks than owning stocks that pay higher dividends?” It’s a reasonable question but the answer lies in the internal rate of growth in the company created by a high reinvestment return.

The chart below shows the internal growth of a company with a Return on Invested Capital (ROIC) of 20% per year with no dividend. Since there is no dividend there are also no taxes to be paid.

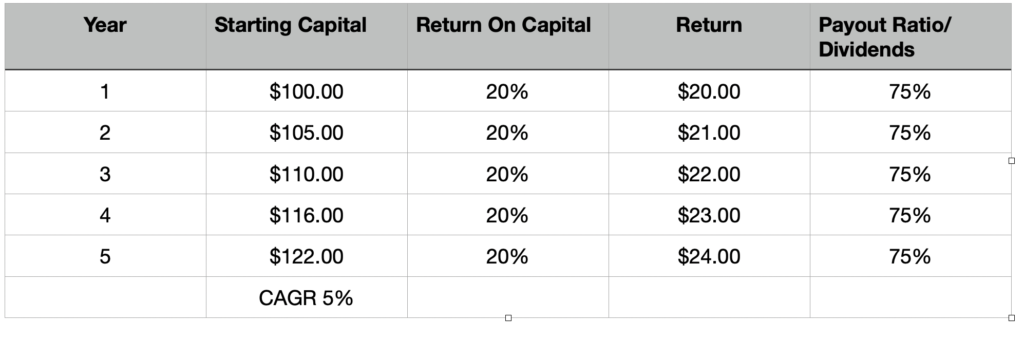

The second chart below shows a company earning the same 20% on its ROIC but pays out 75% of its earnings in the form of dividends. In this example the dividend paying company has Compounded Annual Growth Rate (CAGR) of 5% versus the CAGR of 20% for the zero-dividend company. Not to mention that the dividends could be taxable

Despite this example many of our best holdings do pay dividends. My preference is for companies to pay less than 25% of their net income in the form of dividends.

In the past 30 days, two holdings were sold off with a modest loss and gain. A company may be of the highest quality but if the stock cannot gain or it loses traction a decision has to be made. A company that was sold for a loss can be reconsidered after 30-days. If we repurchase within 30-days we lose any benefit of the tax-loss (for taxable accounts only).

Sales

Accenture ACN: Cost was $308 and sold for $300. Accenture had been downgraded by several brokers as future bookings are weakening. Plus, the most recent earnings were positive but partially due to reduced tax rate.

Monster Beverage MNST: Average cost estimate of $53 and sold for $55. The chairman of Bing Energy beverage passed away recently and Monster will be buying the company. This purchase is the likely cause of the recent price weakness. Growth appears to be slowing. In 2020 their Return on Capital was 31% and in the last 12 months it has dipped to 22%. Monster does not have a Wide Moat so competition could be having an impact.

Buys

Mastercard MA: I’ve used the proceeds from the sales of ACN and MNST to fund the purchases of MA. Mastercard operates as a duopoly with Visa and was in my opinion the best company to own which wasn’t in our portfolios. The reason it was initially left out was its flat trading range for the past 3 1/2 years and the chart below shows it appears to be ending its dormant phase. Due to its high ROIC the value of the company continued to rise internally. Since the stock traded sideways it became a relative value due to internal growth. Over time I’d like to add to MA since our total position is relatively small.

Investment returns for Mastercard are quite special: MA went public 17 years ago and has returned 8353% in that time. The compounded annual growth rate is 29.7%. Since going public 17 years ago MA has outperformed Visa especially since 2016.

“Despite the evolution in the payment space, we think a wide moat surrounds the business and view Mastercard position in the global electronic payments infrastructure as essentially unassailable. (Morning star)

Mastercard is one the best examples of what happens to investment returns when you have a strong and “unassailable” Moat. What drives the price in MA shares is the incredible Return on Invested Capital of 60.8% for the past 12 months. (Source TIKR)

In my opinion Mastercard is another company where it’s never made sense to sell, ever. IMO the best place to look for companies that can deliver relatively smooth long term returns are with companies already doing so.

Update from Barron’s magazine for July 16, 2023:

“Mastercard and Visa have been on a tear and yet their stocks remain cheap. Investors should take the opportunity to scoop up shares according to Nicholas Jasinski writes in this week’s edition of Barrons. Visa’s current valuation multiple is a premium of about 30% over the S&P 500, half the historical average of roughly 60%. The picture is similar for Mastercard – its cheaper relative to the market and its own history than it has been in a while. Nothing appears to have changed for either company to warrant a multiple that low compared with the S&P 500, the author notes.”

Thank you for reading.

Brad Pappas

We’ve updated our Vegan Growth Portfolio model results with the data through July 14, 2023.