Client Letter, October 8, 2018

Quick Summary: The end of an era may be at hand. The rally in bond prices that dates back to 1981 appears to be over. I’m not convinced it’s over for good but that’s an argument to be made later on.

In the meantime, falling bond prices represent a headwind for stocks and could remain so until bond prices find a short term floor. This headwind accelerated the decline in stocks on October 4th and 5th. This prompted me to raise cash from holdings that either had losses or were laggard holdings. A portion of cash was used to purchase hedges to offset any future stock price declines.

It’s most likely that this is just a short or intermediate termed decline in stocks as the long term trend remains firmly in place. Part of the purpose of quick market declines is to make investors fearful and uneasy, one reason we use hedges to cushion declines.

Chart 1: This chart below shows that the long term trend to lower interest rates is being threatened. This can’t be a surprise with the rapidly expanding deficits and very low unemployment. But as I’ve highlighted with arrows: it’s not uncommon for interest rates to rise in the latter stages of the business cycle, only to fall hard when the Fed raises rates enough to trigger recession. I don’t see this time as any different. My best guess is the current bond weakness is a future buying opportunity later in 2019.

Chart 2: Proxy for the 30-Year T-bond is the TLT. The chart below is inverse to Chart 1 above. Any further weakness with a close below $113 could accelerate the bond sell-off which would trigger more stock market weakness in the short term.

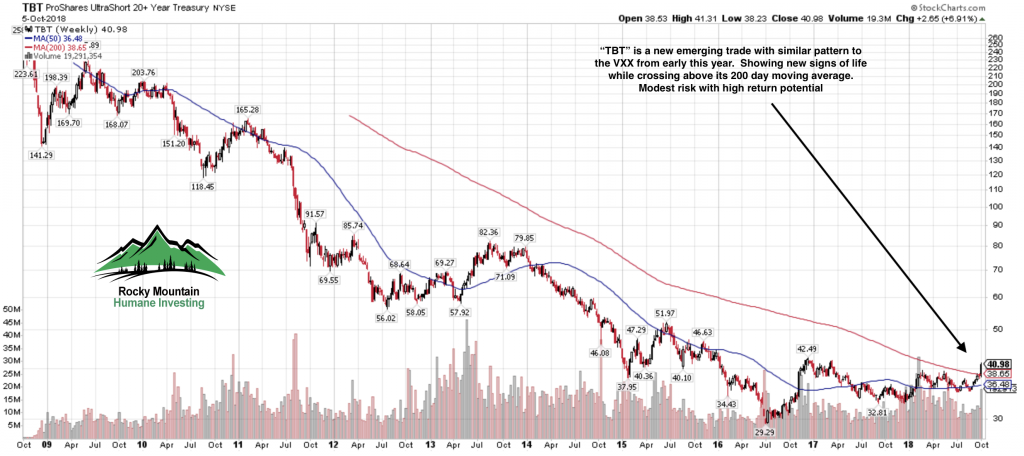

Chart 3: A direct beneficiary of the decline in bond prices is setting itself up for a very good risk/reward trade. As the bond market declines, the TBT will rally higher.

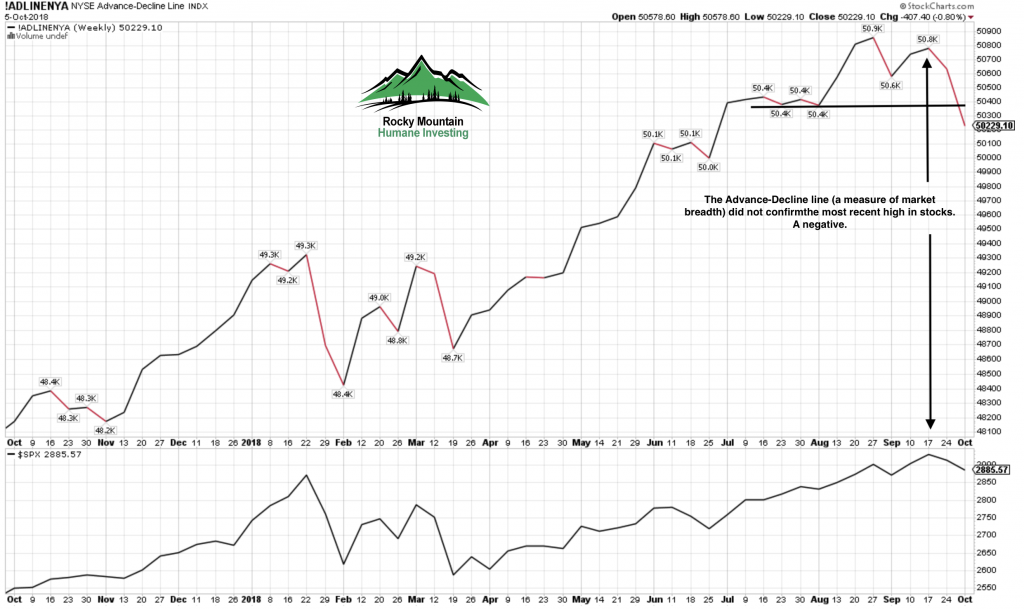

Chart 4: Internal market strength was showing an important discrepancy with the Advance/Decline line which did not confirm the most recent market peak as it should. This non-confirmation gives us a clue that internally at present the stock market is not very healthy and is in need of a purge.

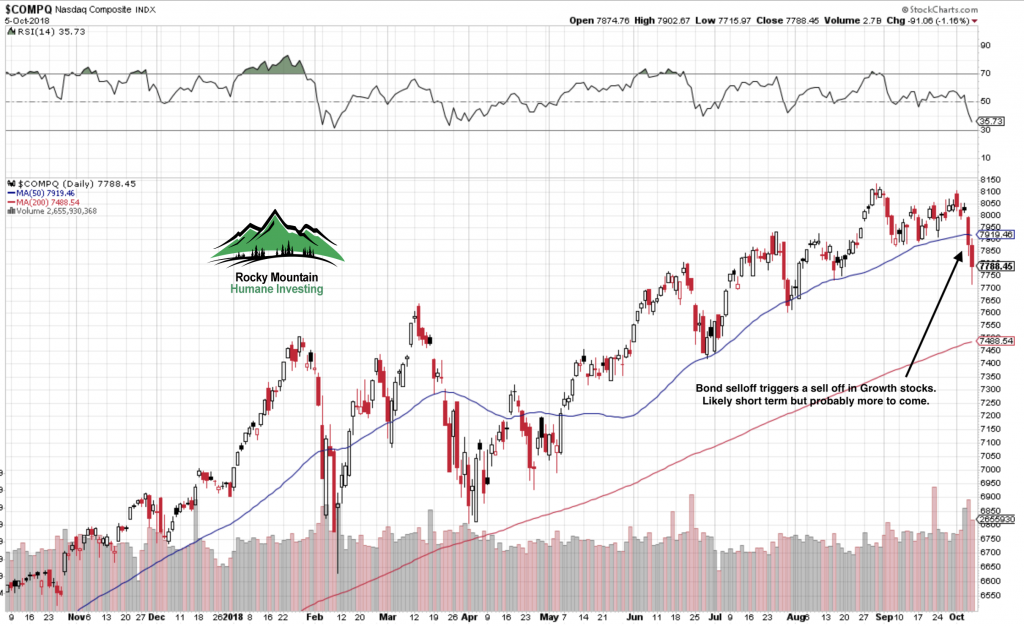

My guess is that the selling is not finished. We may bounce here for a day or two, but if the bond market continues to be weak, the Nasdaq Composite (Chart 5) could visit 7500 or so quickly. Selling would likely be contained at that level. Odds are high this is not the start of a bear market for stocks.

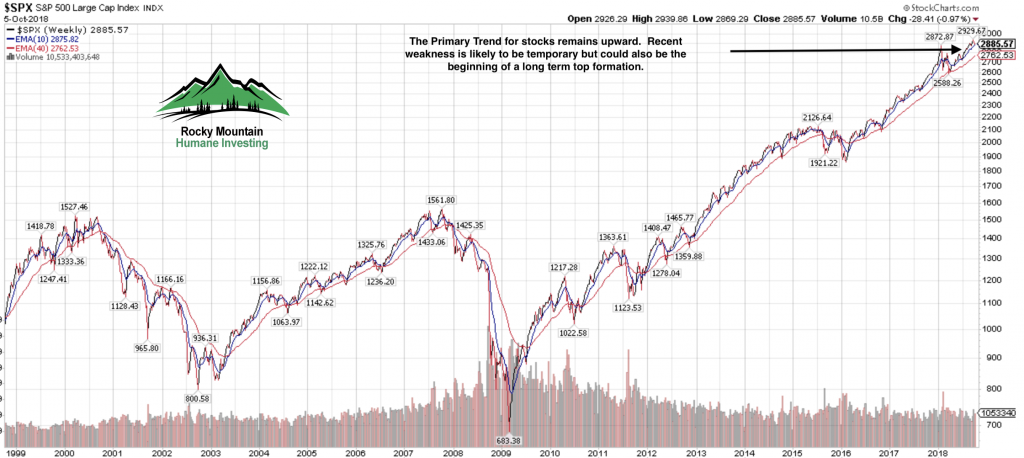

Chart 6: Our long term primary trend indicator remains quite positive at present. Market tops are usually made by a rolling-over process rather than a mountain top peak. See my estimates for business cycle – stock market peak below.

Parlor game guesses for cycle peaks

Based on the Fed’s rate hike projections, we’ll reach inversion by February 2019. The Fed has given no signal to indicate they’ll declare a halt to rate hikes which could push the date to later next year. In fact the most recent jobs data makes me think they’ll hit the brakes hard next year.

So, based on an inversion in February 2019 we can make some recession date assumptions based on the past 9 yield curve inversions dating back to 1957:

The shortest lead time from inversion to recession has been 8 months: October 2019. Median lead time from inversion to recession has been 12 months: February 2020.

Longest lead time from inversion to recession has been 20 months: October 2020.

Understand the recession data is based on NBER declared recessions and they date the start of a recession many months in hindsight. But we can make reasonable estimates based on yield curve inversion dates.

The stock market is a forward looking barometer meaning that the markets look ahead into the future. This means the US stock market will peak and begin to rollover before the recession starts.

Based upon data from 1957, the US stock market has peaked on average 5 months before the start of a recession.

Earliest estimated stock market peak is May 2019. Likeliest estimated stock market peak is September 2019. Latest estimated stock market peak is May 2020.

Thanks again to all of you for your trust. As an investment manager, my goal is to avoid the dogmatic approach, be flexible and neutral to market behavior. Any investor who decides to get into an argument and mansplain to the market will emerged bruised and poorer for the experience.

All the best,

Brad Pappas

The Post Parabolic Blues

4/8/2018

Since the 10% decline in the S&P 500 index in late January I’ve been using my Bull Market playbook to deal with a decline. Technically speaking we are still in a Bull Market but our Bull status is looking more precarious by the day. The Bull Market playbook means I’m looking for a double bottom or retest of the market lows off the initial sell-off. Secondly, I’d be looking to buy stocks on signs of a successful retest and rally.

Friday’s 2.19% decline was especially disheartening since it wiped out three days of gains. Stocks had been showing signs of recovery by trying to build a base from which to rally. Previously, markets were appeased by the story that the White House was using the tariff threats as a negotiating tool. But Friday’s news showed that markets are not buying that story any more. This is a dangerous and unpredictable situation that leaves any investor unhedged in stocks vulnerable to policy mistakes and reckless statements from the White House or cabinet.

The second leg down rallies have been relatively weak with reduced volume while declines have been larger in magnitude and increased volume (not good). This reveals that large institutional investors are in a liquidation mode and are using rallies to sell rather than using declines to accumulate. This is Bear Market behavior and is giving me pause to reassess the likelihood of another another significant leg down for stocks and the possibility of a Bear Market.

Perhaps this weakness is the aftermath of the parabolic rise in stocks earlier this year? Plus the extreme readings of investor sentiment? It’s possible, but I’d argue that stocks and bonds are now reacting accordingly to an aggressive Federal Reserve and a much higher than average possibility of policy mistakes from the White House.

Chart 1

Chart 1 above, courtesy of Carl Swenlin of Decisionpoint, shows the importance of the $257 level for the “SPY” aka S&P 500 ETF. Both the 200 day moving average and the underlying trend line from the 2016 rally converge at nearly the same level.

There are also other important issues the world stock markets are contending with:

The global economic recovery is mature and slowing. Worldwide GDP data is showing clear signs of slowing.

Policy Errors: The tax cuts are the personification of fiscal irresponsibility and there’s no going back.

Trade Wars are “good and easy to win”. Investors aren’t fooled in the least by this rhetoric (see Smoot-Hawley Tariff Act). We’ve never had a President who can just as easily talk up a stock market and talk it down with rhetoric within weeks. This is certainly a market headwind for stocks.

Chart 2

Aggressive Federal Reserve: The “Yield Curve” (shown above in Chart 2) is growing increasingly negative as short term interest rates are rising which will eventually kill the economic expansion. This causes investors to buy long term Treasury bonds. The higher short term yields and lower long term yield flatten the difference between short and long term rates which reduces the incentive for banks to lend.

The Yield Curve is a simple indicator and one of the most powerful tools to predict markets and the economy. Once the curve drops to .5 its “Goodnight Irene” for stocks and “Good Day Sunshine” for Treasury bonds. This is why we’ve recently added long term Treasury bonds to client portfolios.

If you’d like to learn more about the Yield Curve, there is an array of data from none other than the Federal Reserve:

https://www.clevelandfed.org/our-research/indicators-and-data/yield-curve- and-gdp-growth.aspx

Our Present Status: A sharp break in the price in Chart 1 below $257 without a rebound implies there is more selling ahead, which could be significant. Since my style of investing is based on reacting rather than predicting, I’d look for a $257 break to increase our existing hedges and further reduce stock holdings.

Should the price break below $257 not occur or occur briefly, I’d keep the status quo but expect the bottoming process to take longer than expected. I’d likely prefer to reduce stock holdings in strength until we see a positive change in market behavior.

Treasury bonds: My W.A.G. for Treasury Bonds and the economy is that the Yield Curve inverts in 2019 which will cause a full blown bear market in stocks and bull market in Treasury bonds. T-bonds could rally by more than 20% due to the reduced effect of lowering interest rates in an already low rate environment by the Fed. This could be followed by recession and bear market low by 2020.

Bottom Line: I’m agnostic to market direction as we can generate profits in accounts regardless of market trends. It’s the transition periods which we are possibly in that are tricky to assess. Once a new trend emerges, be it up or down, I’ll adapt and do my best to continue generating profits on your behalf.

Thank you,

Brad Pappas

Enjoy The Ride!

10/19/2017

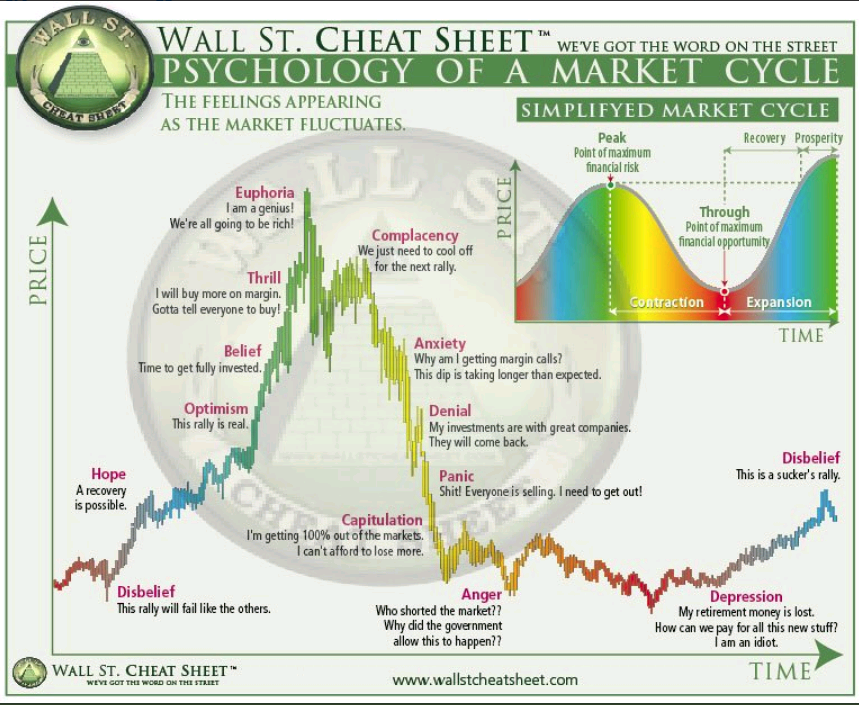

Since the market bottom last November the S&P 500 has rallied from 2083 to 2560, a very healthy gain of 22.8% not including dividends. Despite these gains there are almost no signs of euphoria within the investing community which leads me to think this rally still has a long way to go. Euphoria is a necessary evil that’s almost always seen at major market highs when investors refuse to believe the market will roll over.

Is there a valid case to be Bearish? Yes, but market momentum always takes precedence. Eventually the bears will be right but it may take a few more years and in the meantime so much opportunity will be lost. The bearish arguments have been around for years and completely dismissed as markets make new The bear case always sounds intelligent and well thought out but their losses and opportunities missed can be staggering.

This week marks the 17th time in the past 90 years that stocks made new all-time highs each day of the week. In only ONE instance did this ever mark the exact top of the stock market (1968). Higher highs occurred 94% of the time.

Once a trend has been established it tends to persist and run its full course.

Investing always has some form of anxiety for investors to contend with. If it’s not nervousness with the decline in your account value it’s the fear of the value rising too much and worrying you’ll give it all back. Is there a Goldilocks too hot – too cold – just right equivalence? Nope, but keep things simple as in try to sensibly grow your principal as much as possible in the good years and lose as little as possible in the bad. And, try not to mess it up in the meantime which is why: Temperament can more important than intellect.

In past years bonds offered a decent yield which allowed an investor to gain some income and diversify from stocks. The problem in this era is that yields are very low and in order to gain a modest, even a high single digit return there must be some increase in bond prices and very little of that is happening now.

One of the best books ever written on investing was authored by Jesse Livermore “How to trade in stocks” published in 1940. At his peak Livermore was worth an estimated $100 million in 1929 dollars after starting from scratch. His approach was systematic and still effective today and I use many of the rules he originally created for himself.

One of Livermore’s lessons was: “Money is made by SITTING not trading” To paraphrase, when you know you’re in the right you stay invested until the rally fades. You should remain in the stocks that are trending higher and take small losses along the way (never ride a losing stock down hoping it will turn).

The majority of “easy” money made in stocks is made during two unique phases of the economy/markets: The violent rally higher during the transition from recession to expansion and during long trending rallies in the mid cycle of the expansion like we’re experiencing right now. Smooth trending markets may happen just once or twice in a decade so it’s important to maximize the opportunity when it’s present.

While it’s part of our management philosophy to protect our clients during major down drafts, we do not sell prematurely or pretend that we can call a market top. “Top Calling” the stock market is a way of gaining media exposure and attention. Top Calling has nothing to do with solid investment management since astute advisors know it can’t be done. The better option is to let the market take us out when the time is right with our built in exposure systems.

Charting the warning signs of the 1987 crash

It’s been 30 years since the 1987 crash so why not look at it closely for lessons?

The evolution of market tops is a gradual process whereby markets weaken as selling and distribution increase. Sometimes the flat sideways trend is nothing more than the “pause that refreshes” before another up-leg commences. However, sideways/choppy trends can also be the early stage of something more ominous.

In the summer of ‘87, the bond market was very weak with declining prices and higher yields which were becoming increasingly more attractive to stocks. This was causing a migration from stocks which began to manifest itself in August. These were the grand old days when investors wouldn’t buy a municipal bond unless it had a tax free yield of 10% or more.

Stocks peaked in August then sold off by 8% in September then rallied 6% into October before crashing. The decline in early October breached the 50-100-200 day moving averages which would have triggered a wave of sell signals for us. We always use the 200 day moving average as the ultimate cut off for owning stocks. I consider declines below the 200 day to be Bear Market country.

Summary: Enjoy the ride.

Brad Pappas

970-222-2592

Brad@greeninvestment.com

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Past performance is no guarantee of future results.

The U.S. and World stock markets remain in bull-mode, which was my expectation based on my April 2009 letter. This move up was triggered by data that revealed things were not as bad as the consensus expected which caught the majority by surprise since the sentiment of investors was intensely negative in March. Stock markets are rebounding on par with previous waterfall declines and the emergence of the economy from recession to growth. The lows in March will likely be the lows for decades.

Based upon numerous studies of past waterfall market declines I would expect the stock markets to churn higher as evidence continues to mount confirming the end of the recession which in turn will give investors more confidence. In a complete reversal of last Fall’s sentiment of “Get me out I can’t take it anymore!” we are now hearing “Get me in, I can’t take it anymore!”

Recent data indicates that the U.S. economy is now out of recession and that July will mark the first month of growth. Looking back to previous periods of recession segueing to growth, stock market declines are usually shallow and short of single digits which don’t allow investors an easy entrance. In addition, as Summer turns to Fall “performance anxiety” will start to be a major driver forcing investors and professionals to commit to risk as it will be clear that the Bearish majority opinion favored early this year is clearly out of sync at present. There may a “melt-up” as the anxiety to perform becomes intolerable.

I would caution investors against allowing the fear and risk aversion that was rampant in the past year from coloring their view going forward. The portfolio that was well positioned last year for the crisis will be poorly positioned to handle the economic recovery now forming.

Its extraordinary to watch the talking heads on CNBC wax wondrous about the stock market when the majority of them were cowering under their desks or outright bearish this Spring. Fear is dissipating and a return to risk taking continues as credit spreads shrink. Within the last week Goldman Sachs and Credit Suisse have upped their year-end targets for the S&P 500 to the vicinity of my own target of 1050-1100. While its good to have company, which in turn will instigate more buying pressure, my views on the market rally are no longer in the minority opinion so I must keep an eye out for a potential development that could break the bullish consensus.

The most perplexing question I face at the moment is whether the traditional seasonal market weakness from August to October will occur this year. In past transition years, noticeable market weakness within six months of a transition from recession to expansion is rare. In 2003, which was our last transition year there was no noticeable weakness until 2004, we may see the same lack of pullbacks this time. Typically in post waterfall declines we could expect this current rally to live for at least another six months to early 2010. In contrast, research on market cycles from Ned Davis, which I showed in chart form in April predict a market top in August, leading to weakness thru October followed by a strong rally thru December.

Based on past conference calls with clients there seems to be confusion at how we could be moving to a period of economic expansion with headlines so bleak. So, if you find yourself scratching your head at how we could be moving from recession to expansion I’d like to quote Anirvan Banerji of the Economic Cycle Research Institute:

“Indicators are typically judged by their freshness, not their foresight.”

Generally little context is ever provided to shed light on the data as to whether the data is peaking or not, as to whether a leading, coincident or trailing indicator. For example employment is a lagging data point and typically peaks after the economic trough. The lag time varies considerably from one month (1982) to 19 months (2003).

Stock Selection: Small versus Large: Performance data continues to suggest that our strategy of preference for Small Cap Growth stocks with modest valuations otherwise known as GARP (Growth At A Reasonable Price) has been spot-on. Small GARP stocks out-performance will likely be a long-term, multi-year trend. For example, the average length of Small Cap out-performance versus the S&P 500 since 1926 is 71 months and as of this month I estimate we’re only in month 14.

The effects of a newly expanding economy with increased desire for risk are having a profound impact on our domestic Small Cap Holdings. Our biggest winner of the year has been Global Cash Access LLC (GCA), which we were able to acquire initially at just under $4 a share and has reached $9 a share.

Domestic and Emerging Markets: In addition to our preference for Small Cap stocks, I have significantly increased our exposure to Small Cap Emerging Markets stocks. Emerging Markets have displayed superior relative strength to the U.S., Brazil and Chine in particular. While this performance is a reflection of increased confidence in their ability to manage the downturn, they are also not hindered by a depleted, over-leveraged consumer or anemic GDP growth. With these factors in mind I continue to believe the Emerging Markets have superior risk/reward over the next 2-3 years versus the U.S. markets. I am very concerned that the U.S. stock market may drift sideways for an extended period after our present rally. Diversification into Emerging Markets is a strategy to reduce our dependency upon the U.S. economy and stock market. In fact, one should consider that a significant percentage of our demand expansion in the U.S. is originating and being driven from Asia, specifically China.

The returns from our EM holdings have been beyond my expectations, our holdings in China have been spectacular. Our “Green” holdings in China Green Agriculture (CGA), RINO International (RINO) have exceeded 100%. We were fortunate enough to identify both CGA and RINO before they gained a listing on the NYSE or NASDAQ. Once they received approval to trade on our exchanges their appeal broadened due to the increased exposure to U.S. investors. Benign companies such as China Automotive (CAAS) and Chinacast Education have been outstanding as well and helped to lift accounts back into positive territory after a dismal 1st Quarter. These stocks are not without volatility and saw their valuations decimated in 2008 which created an amazing situation of highly profitable and growing companies priced at rock bottom valuations.

Bonds: As stated in previous client letters Treasury Bonds were due for a decline. Since December, at the height of the credit crisis the Ishares 10-20 year Treasury Bond ETF (symbol TLH) traded at $123 a share but by last month the shares were down to approximately $104 which highlights the risk of following massed emotions during the crisis. Insult to injury to those investors who panicked and sold off their stocks to buy Treasuries. On the other hand we took advantage of the declines in economically sensitive debt which were abandoned during the crisis. Yields on Corporate and Preferred Debt reached 14% to 17% during the late 1st Quarter and have since rebounded to 8% to 13% (yields decline as prices rise).

Treasuries are no longer as unattractive as they were six months ago as the bubble in Treasury prices has popped. If the economic rebound is as anemic as suspected, Treasuries could become a haven against economic weakness. Hence, recent debt purchases have been in high grade Treasuries or TIPS (inflation protected Treasuries).

Potential signs of the end of the rally: Rallies emerging from waterfall declines can exceed in breadth and duration beyond the most optimistic investors, I would not be surprised to see our current rally last through the end of the year without nary a pullback beyond a handful of percentage points. Sometimes the hardest position to take as a strategist is to do nothing….to let the rally run its course.

Premium valuation – If the market were to exceed 18x earnings of $60 a share or 1100 on the S&P 500.

Rising corporate bond interest rates – Since early November the gap between corporate and government bond yields has been shrinking, if this spread were to begin to widen once more it would be cause for concern.

Excessive investor exuberance – Markets do move on psychology and just as the March lows saw investor despondency, sentiment has been steadily improving (or getting worse depending on your point of view due to the inverse nature of psychology) and we must be on the alert for frothy behavior. We are getting close to excessive exuberance but not quite there yet.

2010: It’s my belief that the negative views of the Bears, which are being ignored at present, will manifest themselves in 2010. By no means am I predicting a crash or another bear market, “lackluster” might be a good word to describe the broad indices next year. By 2010 stock market valuations will no longer be cheap, inflation pressures could emerge, or anemic economic growth peters out with the lack of stimulus. By 2010 the economy will be forced to walk on its own legs without the support of massive economic stimulus. Fears of a Double Dip recession with accompanying national debt could emerge which would likely put pressure on stock prices, especially in the US. It would be unwise to assume that economic growth from here will be any more than lumpy, inconsistent and anemic.

Our present rally will continue to assume economic growth into 2010 and 2011. These assumptions could be set the stage for potential disappointment if they fall short. While it feels wonderful now to believe in the potential for growth, investors should keep a balanced view and err on the side conservatism until future market weakness and investor sentiment reaches the point to have factored in lower than average corporate earnings growth next year.

RMHI Blog: In an effort to provide clients with current information regarding market outlook, holdings, etc, I’ve created the RMHI Blog which you’ll be able to view at our new updated website at: www.greeninvestment.com/blog. Its my hope the Blog will bridge the information gap between quarterly letters and give clients a feel for what’s going in the financial universe.

Warmest Regards,

Brad Pappas

July 23, 2009

Rocky Mountain Humane Investing Outlook: April 2009 (Posted July 2009)

“Markets do have a lovely tradition of overshooting themselves both in the upside and downside”: from the RMHI 1st quarter client letter.

Is there a more droll way to describe the emotions of early March? It would have been uncommonly rare to have seen the selloff in late February and early March evolve into a lasting period of price erosion without some sort of quick rebound, only the 1929-31 period showed a lower low after such a devastating waterfall selloff. The selloff in March created a sense of investor despondency and incoming phone calls only seen at major market bottoms. This depression stood in contrast to a string of data points suggesting emerging stability that I wrote of in January:

- “Declining New Lows: On October 11th when the SP500 first reached 850, the number of stocks making new lows exceeded 3000. On January 20th the SP 500 touched 804 and the number of new lows was 186. Despite the SP500 being actually lower than 10/11, the number of stocks making new lows is only a tiny fraction of previous sell-offs. This trend has been apparent since November when the index made what might be the ultimate low for this Bear Market of 740 yet the number of new lows was just 600.” At the March low there was only 855 stocks making new lows, despite the market being 22% below the October low. In addition, volume at the October low was 2.85 billion whereas the March low volume was just 1.56 billion, clearly a marked drop in selling intensity. All major market bottoms showed this behavior.

- “Crude oil prices: Stability in oil prices may mean we’re reaching stability.” Crude oil and other commodities are frequently a barometer of worldwide economic activity. The May futures contract for crude broke out of a downtrend in the third week of February and have rebounded from $40 to $54 a barrel. In addition, industrial use metal Copper broke its downtrend at $1.40 and has rallied to $1.80.

- “Baltic Dry Index: The Baltic Dry Index of shipping rates for container ships has leveled off after a precipitous decline. The Baltic Index is a very good forward indicator of worldwide economic activity. It reflects the prices paid to hire an oceangoing freighter to haul goods or raw materials. In recent years, China has been a driver in pricing with their economic expansion.” While the Baltic Dry index is not an ideal barometer of economic activity in this cycle (a probable glut in oversupply of available ships, causing cheap pricing), the lack of continued price erosion is clear.

- “A roadmap of composite (1929-2002) post-crash DJIA performance. Ned Davis Research has done a fascinating study of post crash declines in excess of 20%. Although the “crash” phase was not the actual end of the Bear Market, the declines were not exceeded either. Retests of the market lows were very common and generally occurred within 90 days of the waterfall selloff. In our case, October 11 would be the 0 date while November 20, 2008 remains the ultimate low of this Bear decline, which perfectly parallels the composite roadmap of this chart. Other points of merit: The waterfall selloff occurred on average of 130 days before the end of the recession, but the markets started to make progress approximately 70 days before the end of the Recession. Based on analyst estimates for the Standard and Poors 500, the approximate end of the recession could be in the 2nd or 3rd quarter of 2009, which coincidently matches Davis’s chart.” While the markets did go to new lows in March, they did not break and with blazing speed erased the March decline in two weeks. Furthermore, my reference to the parallels of 1974 and 1938 continue to look accurate, especially 1938.

Mark Twain said: “History doesn’t repeat itself; at best, it sometimes rhymes.”

Economies and equities have gone through boom and bust cycles many times over the past hundred odd

years. While the reasons for the boom or bust change with each cycle, the reaction of the market place

post-collapse, which is based largely on human psychology and economics reveals a pattern that continues

to rhyme with surprising frequency and accuracy. These patterns of market behavior are most accurate in

the transitional period between Bear and Bull cycles but lose their accuracy once the transition cycle is

over, whereby the markets are on their own and trade according to new incoming data.

In January, I brought this chart to your attention:

“We are in a moment “in-between” of gray twilight between dark and dawn”

In early March we found ourselves in a period of agonizing investor angst yet improving market internals and even more astonishing…….. early signs of economic stability and yes……….improvement. The U.S. Equity market staged a rally with breathtaking swiftness and rebounded from 650 to 830 on the SP500.

In January, Ned Davis Research published a chart that has been uncanny both in terms of market seasonality and behavior and is likely a good road map for 2009. This “road map” is meaningless unless the underlying economic data support the price movement. The March rally has been unique in that it was supported not by government acts but improving economic data, a contrast to the failed rally of November and December.

Ever since the market bottom in October there have been a series of false starts where rallies petered out in a matter of a few short weeks. These rallies were only technical in nature; there was no underlying fundamental reason to support them as the economy remained in freefall. Since the bottom in early March, there have been six 90% upside volume days, a clear difference than the tepid rally in November and most importantly the rally coincided with news from Citigroup, JP Morgan and Bank of America that January and February were profitable.

A cyclical Bull Market to last till late summer, in five steps:

Step One: The composite chart above details a brief “blast off” rally in the range of 18% starting in late

February. These rallies catch everyone by surprise, as they appear to come out of nowhere but do coincide

with bottoms in the economy and investor sentiment. Our rally appears to have peaked at 23% and started

in early March rather than late February.

Step Two: A period of consolidation for the market to digest the move. The market pulls back a bit but

doesn’t break lasting for 4-6 weeks. I believe we’re in this phase now.

Step Three: A 30% rally as investors see further evidence of the economic bottom with the prospects for

the recession ending and stability in housing. This move like Step One is a virtual race to get invested by

an underexposed hedge fund industry and others. In the past 10 recessions, the stock market has staged a

lasting and major bottom on average 4 months before the end of the recession, or mid Summer 2009.

Further argument for the end of the recession by summer will be the effects of the Presidents stimulus

package, which will start to resonate within the economy in the second quarter of 2009. Earnings estimates

by Standard and Poors validate this thesis as well with a quarterly earnings jump from the 1st Q to the 2nd

of $13.00 to $14.96.

Step Four: The pause that refreshes. The months of June-July bring a second gentle period of

consolidation as the gains are digested by trending sideways. Stock market rallies coming out of

recessions are generally always exceptional but they don’t move in a straight line.

Step Five: A midsummer and final rally in the range of another 25% to the normal stock market valuation

of (100 year average) 16 times 2010 earnings of $66 or approximately 1100 on the SP500 by August. A

good chance this will be the high of the year.

I fully realize these figures sound astonishing but we can hardly forget how far we’ve fallen. A rally of this

magnitude actually falls in line with (here’s the rhyme again) 1938 and 1974, which rallied 60% and 51%

respectively. The last emergence from a recession for the stock market was (another rhyme) March 2003

where it staged an unending rally till the end of the year with a trough to peak move exceeding 50%.

The mean cyclical return for the stock market in a secular bear market is 65% over 508 days. In addition,

volatility in the markets today is much greater than in previous periods. Ned Davis’s own estimates are that

the SP 500 could reach 1200-1300 by summer, which would be wonderful. But any rally that extends into

late summer will likely be running out of steam and showing signs of exhaustion and excessive enthusiasm,

this is the stage of the rally where we must be selling. The very same panic-stricken investors who are in

cash now will be rabid to gain exposure as performance envy kicks in. There is substantial career risk for

a portfolio manager to be in cash and show nil or negative returns when market indices are substantially net

positive for the year, the NASDAQ has already returned to positive for the year.

Post Rally: The present rally will be based on the presumption that the economy has bottomed but

investors will not have had the chance to factor in unintended consequences, especially inflation. Its my

guess that inflation will return as an issue but its clearly too early to profit from that at this point in time,

the prospects for deflation need to be cured first along with housing before inflation is a substantial issue.

If inflation remains in check and Treasury bonds remain relatively stable with low yields along with an

economy that shows improvement then the stock market should merely correct itself with the normal

seasonal weakness and not commence a new Bear market. Either way, I plan on sticking to discipline and

having minimal long stock exposure by late summer.

All the best,

Brad Pappas

March 29, 2009